TREYNOR

Updated: 21 December 2012

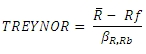

Use TREYNOR to calculate the Treynor ratio based upon return data. You have the option of computing the Treynor ratio using either simple returns or geometric returns. For simple returns, the Treynor ratio is calculated as the mean of the returns minus the risk-free rate divided by the beta of the returns against the benchmark returns.

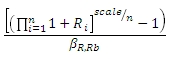

For geometric returns, the Treynor ratio is calculated as the geometric mean of the return minus the risk-free rate divided by the beta of the returns against the benchmark returns. For the sake of consistency, the risk-free rate should be in the same units as the scaling factor.

ßR,Rb = SLOPE(R,Rb)

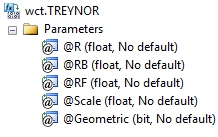

Syntax

Arguments

@R

the return value; the percentage return in floating point format (i.e. 10% = 0.10). @R is an expression of type float or of a type that can be implicitly converted to float.

@RB

the benchmark return value. @RB is an expression of type float or of a type that can be implicitly converted to float.

@RF

the risk-free rate. @RF is an expression of type float or of a type that can be implicitly converted to float.

@Scale

the scaling factor used in the calculation. @Scale is an expression of type float or of a type that can be implicitly converted to float.

@Geometric

identifies whether or not to use geometric returns in the calculation. @Geometric is an expression of type bit or of a type that can be implicitly converted to bit.

Return Type

float

Remarks

· If @Geometric IS NULL then @Geometric is set equal to 'False'.

· If @Scale IS NULL them @Scale is set to 1.

· For daily returns set @Scale = 252.

· For weekly returns set @Scale = 52.

· For monthly returns set @Scale = 12.

· For quarterly returns set @Scale = 4.

· To calculate the Treynor ratio using price data or portfolio values, use the TRYENOR2 aggregate function.

· @Geometric must be the same for all rows in the GROUP BY

· @Scale must the same for all rows in the GROUP BY.

· @Rf must the same for all rows in the GROUP BY.

Examples

In this example we have return data for IBM and we want to calculate the simple Treynor ratio using the S&P 500 returns as a benchmark.

SELECT wct.TREYNOR(r,rb,.001/cast(252 as float),NULL,NULL) as TREYNOR

FROM (VALUES

('IBM','2012-12-18',0.0107,0.0115),

('IBM','2012-12-17',0.0097,0.0119),

('IBM','2012-12-14',-0.0012,-0.0041),

('IBM','2012-12-13',-0.005,-0.0063),

('IBM','2012-12-12',-0.0064,0.0004),

('IBM','2012-12-11',0.0082,0.0065),

('IBM','2012-12-10',0.0035,0.0003),

('IBM','2012-12-07',0.0119,0.0029),

('IBM','2012-12-06',0.0056,0.0033),

('IBM','2012-12-05',-0.0037,0.0016),

('IBM','2012-12-04',-0.0006,-0.0017),

('IBM','2012-12-03',-0.0031,-0.0047),

('IBM','2012-11-30',-0.0076,0.0002),

('IBM','2012-11-29',-0.0023,0.0043),

('IBM','2012-11-28',0.0039,0.0079),

('IBM','2012-11-27',-0.0086,-0.0052),

('IBM','2012-11-26',-0.0032,-0.002),

('IBM','2012-11-23',0.0168,0.013),

('IBM','2012-11-21',0.0058,0.0023),

('IBM','2012-11-20',-0.006,0.0007),

('IBM','2012-11-19',0.0182,0.0199),

('IBM','2012-11-16',0.0059,0.0048),

('IBM','2012-11-15',0.0018,-0.0016),

('IBM','2012-11-14',-0.0149,-0.0139),

('IBM','2012-11-13',-0.0049,-0.004),

('IBM','2012-11-12',-0.0021,0.0001),

('IBM','2012-11-09',-0.0024,0.0017),

('IBM','2012-11-08',-0.0055,-0.0122),

('IBM','2012-11-07',-0.0158,-0.0237),

('IBM','2012-11-06',0.0048,0.0079),

('IBM','2012-11-05',0.0036,0.0022),

('IBM','2012-11-02',-0.0188,-0.0094),

('IBM','2012-11-01',0.0135,0.0109)

)n(ticker,tdate,r,rb)

This produces the following result.

TREYNOR

----------------------

0.000388271591630151

In this example, we use weekly returns and calculate the Treynor ratio using geometric returns.

SELECT wct.TREYNOR(r,rb,.001/cast(52 as float),52,'True') as TREYNOR

FROM (VALUES

('IBM','2012-12-17',0.0173,0.0157),

('IBM','2012-12-10',-0.001,-0.0032),

('IBM','2012-12-03',0.0099,0.0013),

('IBM','2012-11-26',-0.0177,0.005),

('IBM','2012-11-19',0.035,0.0362),

('IBM','2012-11-12',-0.0142,-0.0145),

('IBM','2012-11-05',-0.0153,-0.0243),

('IBM','2012-10-31',0.0008,0.0016),

('IBM','2012-10-22',-0.0005,-0.0148),

('IBM','2012-10-15',-0.0695,0.0032),

('IBM','2012-10-08',-0.0133,-0.0221),

('IBM','2012-10-01',0.0151,0.0141),

('IBM','2012-09-24',0.0072,-0.0133),

('IBM','2012-09-17',-0.004,-0.0038),

('IBM','2012-09-10',0.0367,0.0194),

('IBM','2012-09-04',0.0239,0.0223),

('IBM','2012-08-27',-0.0148,-0.0032),

('IBM','2012-08-20',-0.0171,-0.005),

('IBM','2012-08-13',0.0097,0.0087),

('IBM','2012-08-06',0.0082,0.0107),

('IBM','2012-07-30',0.0108,0.0036),

('IBM','2012-07-23',0.0204,0.0171),

('IBM','2012-07-16',0.0347,0.0043),

('IBM','2012-07-09',-0.0282,0.0016),

('IBM','2012-07-02',-0.0213,-0.0055),

('IBM','2012-06-25',0.0097,0.0203),

('IBM','2012-06-18',-0.0271,-0.0058),

('IBM','2012-06-11',0.0203,0.013),

('IBM','2012-06-04',0.032,0.0373),

('IBM','2012-05-29',-0.0268,-0.0302),

('IBM','2012-05-21',-0.0081,0.0174),

('IBM','2012-05-14',-0.0263,-0.043),

('IBM','2012-05-07',-0.0145,-0.0115),

('IBM','2012-04-30',-0.0088,-0.0244),

('IBM','2012-04-23',0.0361,0.018),

('IBM','2012-04-16',-0.0158,0.006),

('IBM','2012-04-09',-0.013,-0.0199),

('IBM','2012-04-02',-0.0152,-0.0074),

('IBM','2012-03-26',0.0154,0.0081),

('IBM','2012-03-19',-0.0026,-0.005),

('IBM','2012-03-12',0.0269,0.0243),

('IBM','2012-03-05',0.0091,0.0009),

('IBM','2012-02-27',0.0053,0.0028),

('IBM','2012-02-21',0.0224,0.0033),

('IBM','2012-02-13',0.0052,0.0138),

('IBM','2012-02-06',-0.0024,-0.0017),

('IBM','2012-01-30',0.0167,0.0217),

('IBM','2012-01-23',0.0103,0.0007),

('IBM','2012-01-17',0.0523,0.0204),

('IBM','2012-01-09',-0.0185,0.0088)

)n(ticker,tdate,r,rb)

This produces the following result.

TREYNOR

----------------------

0.103411484610504

In this example, we look at monthly returns for several different symbols and group the results by symbol. The bench mark is the S&P 500 and is included in the same table as the other returns.

SELECT *

INTO #s

FROM (VALUES

('IBM','2012-12-03',0.0264),

('IBM','2012-11-01',-0.0186),

('IBM','2012-10-01',-0.0623),

('IBM','2012-09-04',0.0647),

('IBM','2012-08-01',-0.0015),

('IBM','2012-07-02',0.0021),

('IBM','2012-06-01',0.0139),

('IBM','2012-05-01',-0.0646),

('IBM','2012-04-02',-0.0075),

('IBM','2012-03-01',0.0605),

('IBM','2012-02-01',0.0254),

('IBM','2012-01-03',0.0474),

('IBM','2011-12-01',-0.0219),

('MSFT','2012-12-03',0.0259),

('MSFT','2012-11-01',-0.0597),

('MSFT','2012-10-01',-0.041),

('MSFT','2012-09-04',-0.0343),

('MSFT','2012-08-01',0.0527),

('MSFT','2012-07-02',-0.0365),

('MSFT','2012-06-01',0.048),

('MSFT','2012-05-01',-0.0823),

('MSFT','2012-04-02',-0.0076),

('MSFT','2012-03-01',0.0164),

('MSFT','2012-02-01',0.0818),

('MSFT','2012-01-03',0.1374),

('MSFT','2011-12-01',0.0149),

('GOOG','2012-12-03',0.0311),

('GOOG','2012-11-01',0.0266),

('GOOG','2012-10-01',-0.0983),

('GOOG','2012-09-04',0.1013),

('GOOG','2012-08-01',0.0823),

('GOOG','2012-07-02',0.0912),

('GOOG','2012-06-01',-0.0014),

('GOOG','2012-05-01',-0.0397),

('GOOG','2012-04-02',-0.0567),

('GOOG','2012-03-01',0.0372),

('GOOG','2012-02-01',0.0657),

('GOOG','2012-01-03',-0.1019),

('GOOG','2011-12-01',0.0776),

('AAPL','2012-12-03',-0.1008),

('AAPL','2012-11-01',-0.0124),

('AAPL','2012-10-01',-0.1076),

('AAPL','2012-09-04',0.0028),

('AAPL','2012-08-01',0.0939),

('AAPL','2012-07-02',0.0458),

('AAPL','2012-06-01',0.0109),

('AAPL','2012-05-01',-0.0107),

('AAPL','2012-04-02',-0.026),

('AAPL','2012-03-01',0.1053),

('AAPL','2012-02-01',0.1883),

('AAPL','2012-01-03',0.1271),

('AAPL','2011-12-01',0.0597),

('ORCL','2012-12-03',0.0653),

('ORCL','2012-11-01',0.0353),

('ORCL','2012-10-01',-0.0099),

('ORCL','2012-09-04',-0.006),

('ORCL','2012-08-01',0.048),

('ORCL','2012-07-02',0.0187),

('ORCL','2012-06-01',0.122),

('ORCL','2012-05-01',-0.0996),

('ORCL','2012-04-02',0.0104),

('ORCL','2012-03-01',-0.0035),

('ORCL','2012-02-01',0.0373),

('ORCL','2012-01-03',0.102),

('ORCL','2011-12-01',-0.1818),

('SP500','2012-12-03',0.0139),

('SP500','2012-11-01',0.0028),

('SP500','2012-10-01',-0.0198),

('SP500','2012-09-04',0.0242),

('SP500','2012-08-01',0.0198),

('SP500','2012-07-02',0.0126),

('SP500','2012-06-01',0.0396),

('SP500','2012-05-01',-0.0627),

('SP500','2012-04-02',-0.0075),

('SP500','2012-03-01',0.0313),

('SP500','2012-02-01',0.0406),

('SP500','2012-01-03',0.0436),

('SP500','2011-12-01',0.0085)

)n(ticker,tdate,r)

SELECT s1.ticker

,wct.TREYNOR(s1.r,s2.r,.001/cast(12 as float),12,'True') as TREYNOR

FROM #s s1

LEFT JOIN #s s2

ON s2.tdate = s1.tdate

AND s2.ticker = 'SP500'

AND s2.ticker != s1.ticker

GROUP BY s1.ticker

This produces the following result.

ticker TREYNOR

------ ----------------------

AAPL 0.209613130538218

GOOG 0.229680999398903

IBM 0.0429792768480309

MSFT 0.054955541570367

ORCL 0.0595638829579447

SP500 NULL

See Also