EQVOLATILITY

Updated: 04 November 2013

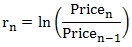

Use EQVOLATILITY to calculate the historical volatility based upon price or valuation data. The historic volatility is calculated as the sample standard deviation of the natural logarithm of the returns multiplied by the square root of the scaling factor supplied to the function. The returns are calculated on the ordered set of data passed as the current price divided by the previous price.

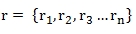

Where

and

Syntax

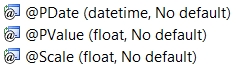

Arguments

@PDate

the date associated with the price or valuation. @PDate is an expression of type datetime or of a type that can be implicitly converted to datetime.

@PValue

the price or value. @PValue is an expression of type float or of a type that can be implicitly converted to float.

@Scale

the scaling factor used in the calculation. @Scale is an expression of type float or of a type that can be implicitly converted to float.

Return Type

float

Remarks

· If @Scale IS NULL them @Scale is set to 252.

· For daily returns set @Scale = 252.

· For weekly returns set @Scale = 52.

· For monthly returns set @Scale = 12.

· For quarterly returns set @Scale = 4.

· @Scale must the same for all rows in the GROUP BY.

· If there are multiple rows for the same date, the @PValue is accumulated.

· The return values are automatically calculated by putting the @PValue in @PDate order.

Examples

In this example we have price data for IBM and we want to calculate the historic volatility for all the rows.

SELECT wct.EQVOLATILITY(

CAST(tdate as datetime)--@PDate

, pr --@PValue

, 252 --@Scale

) as EQVOLATILITY

FROM (VALUES

('IBM','2012-12-18',195.69),

('IBM','2012-12-17',193.62),

('IBM','2012-12-14',191.76),

('IBM','2012-12-13',191.99),

('IBM','2012-12-12',192.95),

('IBM','2012-12-11',194.2),

('IBM','2012-12-10',192.62),

('IBM','2012-12-07',191.95),

('IBM','2012-12-06',189.7),

('IBM','2012-12-05',188.65),

('IBM','2012-12-04',189.36),

('IBM','2012-12-03',189.48),

('IBM','2012-11-30',190.07),

('IBM','2012-11-29',191.53),

('IBM','2012-11-28',191.98),

('IBM','2012-11-27',191.23),

('IBM','2012-11-26',192.88),

('IBM','2012-11-23',193.49),

('IBM','2012-11-21',190.29),

('IBM','2012-11-20',189.2),

('IBM','2012-11-19',190.35),

('IBM','2012-11-16',186.94),

('IBM','2012-11-15',185.85),

('IBM','2012-11-14',185.51),

('IBM','2012-11-13',188.32),

('IBM','2012-11-12',189.25),

('IBM','2012-11-09',189.64),

('IBM','2012-11-08',190.1),

('IBM','2012-11-07',191.16),

('IBM','2012-11-06',194.22),

('IBM','2012-11-05',193.29),

('IBM','2012-11-02',192.59),

('IBM','2012-11-01',196.29),

('IBM','2012-10-31',193.68)

)n(ticker,tdate,pr)

This produces the following result.

EQVOLATILITY

----------------------

0.141437834070616

In this example, we have multiple tickers and we want to calculate the historic volatility for each ticker.

SELECT *

INTO #tbl1

FROM (VALUES

('FB','2013-10-30',49.01)

,('FB','2013-10-29',49.4)

,('FB','2013-10-28',50.23)

,('FB','2013-10-25',51.95)

,('FB','2013-10-24',52.45)

,('FB','2013-10-23',51.9)

,('FB','2013-10-22',52.68)

,('FB','2013-10-21',53.85)

,('FB','2013-10-18',54.22)

,('FB','2013-10-17',52.21)

,('FB','2013-10-16',51.14)

,('FB','2013-10-15',49.5)

,('FB','2013-10-14',49.51)

,('FB','2013-10-11',49.11)

,('FB','2013-10-10',49.05)

,('FB','2013-10-09',46.77)

,('FB','2013-10-08',47.14)

,('FB','2013-10-07',50.52)

,('FB','2013-10-04',51.04)

,('FB','2013-10-03',49.18)

,('FB','2013-10-02',50.28)

,('FB','2013-10-01',50.42)

,('FB','2013-09-30',50.23)

,('ORCL','2013-10-30',33.53)

,('ORCL','2013-10-29',33.71)

,('ORCL','2013-10-28',33.14)

,('ORCL','2013-10-25',33.15)

,('ORCL','2013-10-24',33.07)

,('ORCL','2013-10-23',32.7)

,('ORCL','2013-10-22',32.9)

,('ORCL','2013-10-21',32.95)

,('ORCL','2013-10-18',32.9)

,('ORCL','2013-10-17',32.87)

,('ORCL','2013-10-16',33.02)

,('ORCL','2013-10-15',32.75)

,('ORCL','2013-10-14',33.28)

,('ORCL','2013-10-11',33.26)

,('ORCL','2013-10-10',32.99)

,('ORCL','2013-10-09',32.19)

,('ORCL','2013-10-08',32.37)

,('ORCL','2013-10-07',32.84)

,('ORCL','2013-10-04',33.21)

,('ORCL','2013-10-03',33.12)

,('ORCL','2013-10-02',33.56)

,('ORCL','2013-10-01',33.38)

,('ORCL','2013-09-30',33.05)

,('MSFT','2013-10-30',35.54)

,('MSFT','2013-10-29',35.52)

,('MSFT','2013-10-28',35.57)

,('MSFT','2013-10-25',35.73)

,('MSFT','2013-10-24',33.72)

,('MSFT','2013-10-23',33.76)

,('MSFT','2013-10-22',34.58)

,('MSFT','2013-10-21',34.99)

,('MSFT','2013-10-18',34.96)

,('MSFT','2013-10-17',34.92)

,('MSFT','2013-10-16',34.64)

,('MSFT','2013-10-15',34.49)

,('MSFT','2013-10-14',34.45)

,('MSFT','2013-10-11',34.13)

,('MSFT','2013-10-10',33.76)

,('MSFT','2013-10-09',33.07)

,('MSFT','2013-10-08',33.01)

,('MSFT','2013-10-07',33.3)

,('MSFT','2013-10-04',33.88)

,('MSFT','2013-10-03',33.86)

,('MSFT','2013-10-02',33.92)

,('MSFT','2013-10-01',33.58)

,('MSFT','2013-09-30',33.28)

,('AAPL','2013-10-30',524.9)

,('AAPL','2013-10-29',516.68)

,('AAPL','2013-10-28',529.88)

,('AAPL','2013-10-25',525.96)

,('AAPL','2013-10-24',531.91)

,('AAPL','2013-10-23',524.96)

,('AAPL','2013-10-22',519.87)

,('AAPL','2013-10-21',521.36)

,('AAPL','2013-10-18',508.89)

,('AAPL','2013-10-17',504.5)

,('AAPL','2013-10-16',501.11)

,('AAPL','2013-10-15',498.68)

,('AAPL','2013-10-14',496.04)

,('AAPL','2013-10-11',492.81)

,('AAPL','2013-10-10',489.64)

,('AAPL','2013-10-09',486.59)

,('AAPL','2013-10-08',480.94)

,('AAPL','2013-10-07',487.75)

,('AAPL','2013-10-04',483.03)

,('AAPL','2013-10-03',483.41)

,('AAPL','2013-10-02',489.56)

,('AAPL','2013-10-01',487.96)

,('AAPL','2013-09-30',476.75)

,('IBM','2013-10-30',180.15)

,('IBM','2013-10-29',182.12)

,('IBM','2013-10-28',177.35)

,('IBM','2013-10-25',176.85)

,('IBM','2013-10-24',177.8)

,('IBM','2013-10-23',175.77)

,('IBM','2013-10-22',174.97)

,('IBM','2013-10-21',172.86)

,('IBM','2013-10-18',173.78)

,('IBM','2013-10-17',174.83)

,('IBM','2013-10-16',186.73)

,('IBM','2013-10-15',184.66)

,('IBM','2013-10-14',186.97)

,('IBM','2013-10-11',186.16)

,('IBM','2013-10-10',184.77)

,('IBM','2013-10-09',181.32)

,('IBM','2013-10-08',178.72)

,('IBM','2013-10-07',182.01)

,('IBM','2013-10-04',184.1)

,('IBM','2013-10-03',183.86)

,('IBM','2013-10-02',184.96)

,('IBM','2013-10-01',186.38)

,('IBM','2013-09-30',185.18)

)n(ticker,tdate,price)

SELECT ticker

,wct.EQVOLATILITY(cast(tdate as datetime),price, 252) as VOL

FROM #tbl1

GROUP BY ticker

This produces the following result.

ticker VOL

------ ----------------------

AAPL 0.187965609662433

FB 0.417191302857349

IBM 0.290730860152208

MSFT 0.249263738730003

ORCL 0.161520549212189

Using the same date as the previous example, we can calculate the historical volatility for the last 5 days (which requires 6 days of prices) simply by adding a WHERE clause.

SELECT ticker

,wct.EQVOLATILITY(cast(tdate as datetime),price, 252) as VOL

FROM #tbl1

WHERE tdate between wct.BUSINESSDATE(CAST('2013-10-30' as datetime),'D',-5,'P','') AND CAST('2013-10-30' as datetime)

GROUP BY ticker

This produces the following result.

ticker VOL

------ ----------------------

AAPL 0.279520698602733

FB 0.253546334476966

IBM 0.23412325718261

MSFT 0.423597750600135

ORCL 0.143389046882403