ODDFPRICE

Updated: 31 May 2014

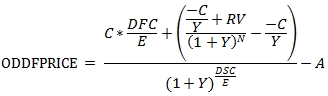

Use ODDFPRICE to calculate the price per $100 face value of a security with an odd first period. The ODDFPRICE formula for a bond with an odd short first coupon is:

Where

A = C * accrued days / E

C = 100 * coupon rate / frequency

DFC = the number of days from the issue date to the first coupon date

DSC = number of days from settlement to coupon

E = the number of days in the quasi-coupon period

N = the number of coupons between the first coupon date and the maturity date

RV = redemption value

Y = yield / frequency

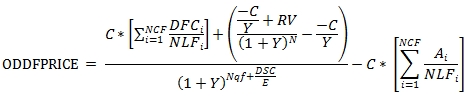

The ODDFPRICE formula for a bond with an odd long first coupon is:

Where

Ai = number of accrued days for the ith quasi-coupon period

C = 100 * coupon rate / frequency

DFCi = number of days from the issue date to the first quasi-coupon date (i=1) or the number of days in the quasi-coupon period (i>1).

DSC = number of days from settlement date to the next quasi-coupon date or first coupon date.

E = number of days in the quasi-coupon period in which settlement occurs

N = the number of coupons between the first coupon date and the maturity date

NCF = number of quasi-coupon periods that fit in the odd period

NLFi = normal length in days of the full ith quasi-coupon period within the odd period.

Nqf = the number of whole quasi-coupon periods between the settlement date and the first coupon.

RV = redemption value

Y = yield / frequency

Syntax

SELECT [wctFinancial].[wct].[ODDFPRICE](

<@Settlement, datetime,>

,<@Maturity, datetime,>

,<@Issue, datetime,>

,<@First_coupon, datetime,>

,<@Rate, float,>

,<@Yld, float,>

,<@Redemption, float,>

,<@Frequency, float,>

,<@Basis, nvarchar(4000),>)

Arguments

@Settlement

the settlement date of the security. @Settlement is an expression that returns a datetime or smalldatetime value, or a character string in date format.

@Maturity

the maturity date of the security. @Maturity is an expression that returns a datetime or smalldatetime value, or a character string in date format.

@Issue

the issue date of the security; the date from which the security starts accruing interest. @Issue is an expression that returns a datetime or smalldatetime value, or a character string in date format.

@First_coupon

the first coupon date of the security. The period from the issue date until the first coupon date defines the odd interest period. All subsequent coupon dates are assumed to occur at regular periodic intervals as defined by @Frequency. @First_coupon is an expression that returns a datetime or smalldatetime value, or a character string in date format.

@Rate

the security’s annual coupon rate. @Rate is an expression of type float or of a type that can be implicitly converted to float.

@Yld

the security’s annual yield. @Yld is an expression of type float or of a type that can be implicitly converted to float.

@Redemption

the security’s redemption value per 100 face value. @Redemption is an expression of type float or of a type that can be implicitly converted to float.

@Frequency

the number of coupon payments per year. For annual payments, @Frequency = 1; for semi-annual, @Frequency = 2; for quarterly, @Frequency = 4; for bimonthly @Frequency = 6; for monthly, @Frequency = 12. For bonds with @Basis = 'A/364' or 9, you can enter 364 for payments made every 52 weeks, 182 for payments made every 26 weeks, 91 for payments made every 13 weeks, 28 for payments made every 4 weeks, 14 for payments made every 2 weeks, and 7 for weekly payments. @Frequency is an expression of type float or of a type that can be implicitly converted to float.

@Basis

is the type of day count to use. @Basis is an expression of the character string data type category.

|

@Basis

|

Day count basis

|

|

0, 'BOND'

|

US (NASD) 30/360

|

|

1, 'ACTUAL'

|

Actual/Actual

|

|

2, 'A360'

|

Actual/360

|

|

3, 'A365'

|

Actual/365

|

|

4, '30E/360 (ISDA)', '30E/360', 'ISDA', '30E/360 ISDA', 'EBOND'

|

European 30/360

|

|

5, '30/360', '30/360 ISDA', 'GERMAN'

|

30/360 ISDA

|

|

6, 'NL/ACT'

|

No Leap Year/ACT

|

|

7, 'NL/365'

|

No Leap Year /365

|

|

8, 'NL/360'

|

No Leap Year /360

|

|

9, 'A/364'

|

Actual/364

|

|

10, 'BOND NON-EOM'

|

US (NASD) 30/360 non-end-of-month

|

|

11, 'ACTUAL NON-EOM'

|

Actual/Actual non-end-of-month

|

|

12, 'A360 NON-EOM'

|

Actual/360 non-end-of-month

|

|

13, 'A365 NON-EOM'

|

Actual/365 non-end-of-month

|

|

14, '30E/360 NON-EOM', '30E/360 ICMA NON-EOM', 'EBOND NON-EOM'

|

European 30/360 non-end-of-month

|

|

15, '30/360 NON-EOM', '30/360 ISDA NON-EOM', 'GERMAN NON-EOM'

|

30/360 ISDA non-end-of-month

|

|

16, 'NL/ACT NON-EOM'

|

No Leap Year/ACT non-end-of-month

|

|

17, 'NL/365 NON-EOM'

|

No Leap Year/365 non-end-of-month

|

|

18, 'NL/360 NON-EOM'

|

No Leap Year/360 non-end-of-month

|

|

19, 'A/364 NON-EOM'

|

Actual/364 non-end-of-month

|

Return Type

float

Remarks

· If @Settlement is NULL then @Settlement = GETDATE().

· If @Rate is NULL then @Rate = 0.

· If @Yield is NULL then @Yield = 0.

· If @Redemption is NULL then @Redemption = 100.

· If @Frequency is NULL then @Frequency = 2.

· If @Basis is NULL then @Basis = 0.

· If @Frequency is any number other than 1, 2, 4, 6 or 12, or for @Basis = 'A/364' any number other than 1, 2, 4, 6, or 12 as well as 7, 14, 28, 91, 182, or 364 ODDFPRICE returns an error.

· If @Basis is invalid (see above list), ODDFPRICE returns an error.

· If @Settlement >= @First_coupon then ODDFPRICE calls the PRICE function.

· If @Maturity is NULL then an error is returned.

· If @Issue is NULL then an error is returned.

· If @First_coupon is NULL then an error is returned.

Examples

This bond has an odd short first coupon (meaning that the first coupon period is shorter than a normal coupon period) and settles on the issue date.

SELECT

wct.ODDFPRICE(

'2014-05-01', --@Settlement

'2034-06-15', --@Maturity

'2014-05-01', --@Issue

'2014-06-15', --@FirstCoupon

0.025, --@Rate

0.0276, --@Yield

100, --@Redemption

2, --@Frequency

1 --@Basis

) as ODDFPRICE

This produces the following result.

ODDFPRICE

----------------------

96.0075631077824

This bond has odd long first coupon (meaning that the first coupon period is longer than a normal coupon period) and settles on the issue date.

SELECT

wct.ODDFPRICE(

'2014-05-01', --@Settlement

'2034-06-15', --@Maturity

'2014-05-01', --@Issue

'2014-12-15', --@FirstCoupon

0.025, --@Rate

0.0276, --@Yield

100, --@Redemption

2, --@Frequency

1 --@Basis

) as ODDFPRICE

This produces the following result.

ODDFPRICE

----------------------

96.0033702877755

Here we calculate the price of a bond with an odd short first coupon with semi-annual coupons payable on March 30th and September 30th.

SELECT

wct.ODDFPRICE(

'2014-03-15', --@Settlement

'2034-09-30', --@Maturity

'2014-03-01', --@Issue

'2014-03-30', --@FirstCoupon

0.0257, --@Rate

0.0269, --@Yield

100, --@Redemption

2, --@Frequency

11 --@Basis

) as ODDFPRICE

This produces the following result.

ODDFPRICE

----------------------

98.1162077824376

Here's an example of the price calculation with a negative yield.

SELECT

wct.ODDFPRICE(

'2014-03-15', --@Settlement

'2024-09-30', --@Maturity

'2014-03-01', --@Issue

'2014-03-30', --@FirstCoupon

0.0157, --@Rate

-0.00235, --@Yield

100, --@Redemption

2, --@Frequency

11 --@Basis

) as ODDFPRICE

This produces the following result.

ODDFPRICE

----------------------

119.276365447988

This is an example of a bond paying interest every 26 weeks.

SELECT

wct.ODDFPRICE(

'2014-10-04', --@Settlement

'2029-12-12', --@Maturity

'2014-03-26', --@Issue

'2014-12-31', --@FirstCoupon

0.1250, --@Rate

0.1100, --@Yield

100, --@Redemption

182, --@Frequency

9 --@Basis

) as ODDFPRICE

This produces the following result.

ODDFPRICE

----------------------

110.842432897841

See Also